Comio exits India. More to follow?

- Ajay Sharma

- Nov 27, 2018

- 6 min read

My insights on how to hedge risks in this volatile Indian smartphone market.

Got this news yesterday of #Comio abruptly closing its operations in India with the Chinese brand owners allegedly absconding, leaving the Indian team and partners high and dry. (This news now also stands confirmed in one of the posts by Sanjay Kalirona in a Whatsapp group).

A very sad thing to have happened, as it will affect thousands of people attached to the brand directly or indirectly. The damage is wide spread – from the manufacturing partners to the Indian team – both on and off-rolls, to the distributors and the retailers, all the way to the service centre owners. It’s a pandemonium!

Since they have been in operation for close to a year now, there will be issues related to stocks in factories/in channel, pending claims, disbursement of salaries, of customer complaints to spare parts’ availability at service centres.

Comio is the third such brand starting with #LeEco followed by #Gionee that has landed in a soup in India. So let us try and analyse the core issues.

For me there are 3 core issues:

1. WRONG UNDERSTANDING OF THE INDIAN MARKET

With the Chinese smartphone market being saturated and the success of select Chinese brands pulling down the home brands, the stakes are high when it comes to India as a market they want to make a dent to. Especially with the country being world’s 2nd largest smartphone market. I am sure every brand that’s coming in knows the competitiveness of the market today vis a vis the time when the brands which have survived till date had initially entered. Those were relatively much better times. However, despite knowing the volatility of the Indian market, the new entrants want to enter India quickly with either none or a shallow short/long term strategy.

To some extent I would also blame the Indian teams who show a rosy picture to them for whatever reasons. By the time the reality sets in, it’s a little too late to jump off the dragon.

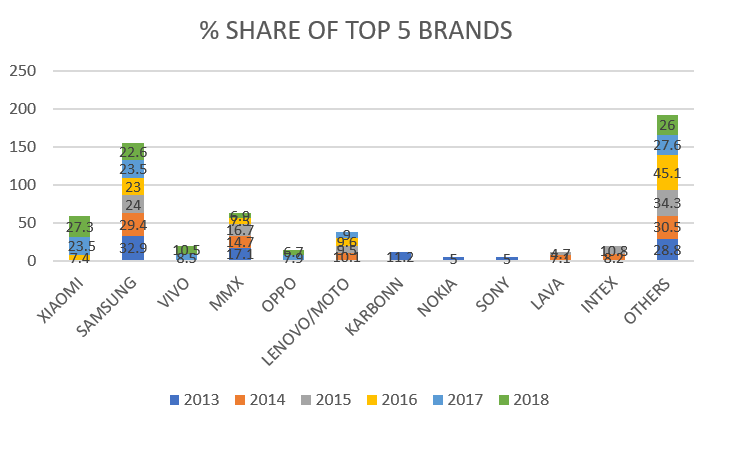

If I were to talk about top 5 brands from the last 5 years (taking Q3 as base each year), the total count of the brands that have had the luxury to be present in the space would not exceed 12. #Samsung is the only brand that has appeared in top 5 for these five years. #Lenovo/Motorola have appeared 4 times, with the last time being in 2017. While #Micromax appeared 5 times, with the last for them being back in 2016, it should be treated as 4 only – Q3 2018 figures are due to the Chhattisgarh project. All other brands are limited to 2-3 times only.

It is apparent that 4 key brands – #Xiaomi, Samsung, #Oppo/#Realme and #Vivo will occupy 4 of the 5 spots, and will not let go off of easily. The fifth is open and could be taken by #Huawei or Lenovo/Motorola or #Transsion in the short term. Though the race is going to be indeed a demanding one.

From Xiaomi to Transsion, out of these 8 brands, to be honest, I think it is only brand no. 1 and 2 which make money in India. The rest are losing.

Data shows that to be the No. 5, one needs to have a share of at least 6-7% approx., which would mean 8 to 9 million smartphones a year which is a pretty mean task today. And if 3 out of the top 5 don’t make money, any new brand coming in will not be able to as well.

Since the top 7 in India – Xiaomi, Samsung, Vivo, Oppo, Huawei, Lenovo/Moto, Transsion are all in the top 10 globally as well, as per IDC Q2 2018 data, they may lose the battle in the short run but will hope for winning the war. They do have the money power to sustain for sometime.

So I foresee the situation of the Chinese brands entering India with no top 10 legacy behind them as very risky.

Data as per IDC. See attachment below.

2. CONSOLIDATION

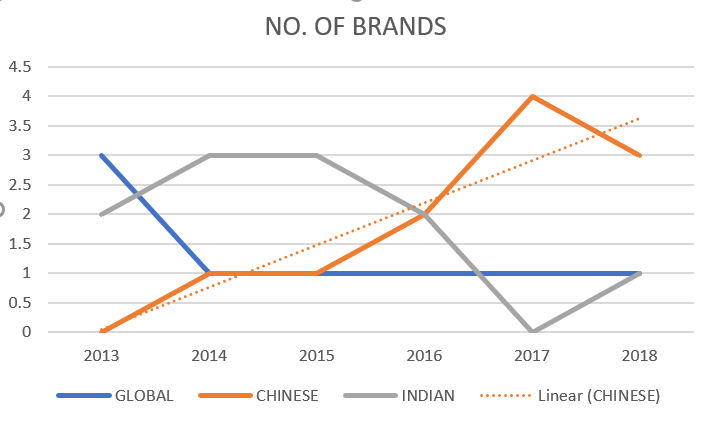

If one has to see the contribution of ‘Others’ as per #IDC data for Q3 in the last 6 years, one will see a reasonably consolidated market initially till 2015, a fragmented market in 2016 with the entry of Xiaomi and Indian brands slipping and again a consolidation from 2017 year on year. Xiaomi came in top 5 in 2016 and Oppo and Vivo in 2017. Samsung has been reasonably steady in these 3 years, Xiaomi has grown exponentially, Vivo is growing though slowly. Oppo may have lost a bit but will catch up with the launch if Realme sooner than later. Lenovo/Moto, Huawei or Transsion can only grow from here and the others’ share will continue to decline making it more difficult.

See Attachment below.

3. EXITS AND ENTRIES

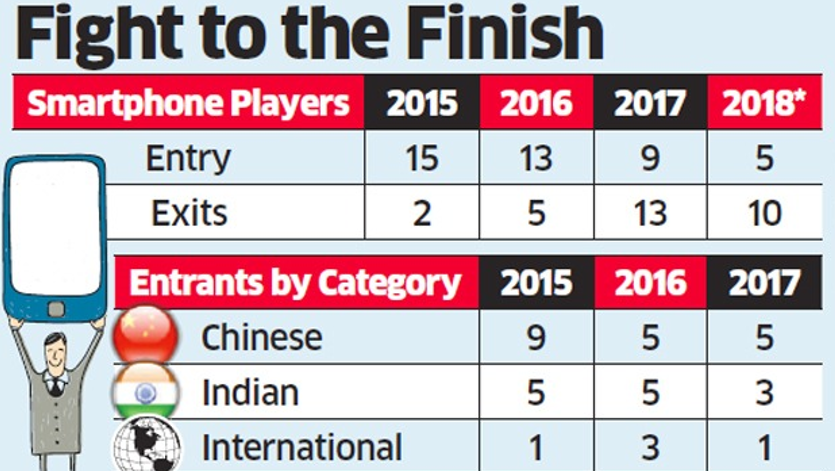

The data may be slightly old but is revealing. The exits are higher than the entries. So possibly brands entering now should know what they are getting into. One needs to be clear if they are just entering to offload their stocks or have long-term plans.

See #Counterpoint attachment below.

CONCLUSION

While each one of you are free to decide on the brand portfolio that works best for you, I’ll list down my suggestions on what to consider while taking up distribution of old and new brands.

Green Zone: 5 brands – Xiaomi, Samsung, Vivo, Oppo/Realme and Huawei. These brands talk volumes and are relatively stable. Good to be associated with them now and in near future.

Yellow Zone: Apple, Transsion and #Nokia. Good to be associated with these brands to some extent now and hope for an improvement later.

Do keep in mind that #Apple plays in a niche segment where the volumes are low. The brand is raising ASP (Average Selling Price) every year, which is reducing its volumes, and not yet clear on its distribution strategy. But it’s still worth doing something with Apple being on your side.

Nokia I believe is rising slowly and steadily without creating much noise and has come in the top 10 globally in less than 2 years. Should grow as they hold a lot of patents, good products and a good team.

Orange Zone: Lenovo/Moto, #ZTE and a couple of Indian brands.

Better to wait and watch in the case of Lenovo/Moto to some extent and ZTE to a slightly greater to understand their focus and strategy for the Indian market. This is not to say don’t touch them but then do apply due diligence.

Only 1-2 Indian brands may survive and exposure to them should be limited to the sub Rs 6k-specifically sub Rs. 5k price segment where the global or chinese brands do not play, except maybe Xiaomi with 1 model.

Red Zone: All other brands specially new ones which are not even in top 10 in China, if not globally – be it C(Gone),G, H, M,T,V and some more which I may have missed.

Do some research on them, talk to people, meet them personally in their office, ask them to show their vision, their expectations from you, the product road map, the R&D facilities that they have in backend, the supports they will give, the leadership team’s understanding of the Indian market, the investments they will make with timelines specially the initial ones not in words but a break up, the Indian leadership team and their past track record. Start slow and steady. If they say we will invest with growth, tell them the same applies to the partners as well. The correct strategy would be to invest based on seeing the investments from the company.

Better to lose profits than to lose the principal amount.

Please don’t get me wrong. Not all brands which are new and not in top 10 globally or in China are unsafe. Some maybe good, even maybe better than how I’ve analysed them and not even covered them.

After all, many of the partners are financially strong, waiting for the right opportunity and willing to take a chance. They may understand things better than me. But then no harm in applying due diligence.

For my Indian friends – Don’t get swayed with a job to the extent that you hit your own career later if things go wrong and lose your credibility in a desperate move to get a job

by overselling. Most of you are young and have long careers ahead of you. One wrong move and you will lose your credibility built over years.

I wish you all the best.

Great Analysis ! Must read article for the industry . Keep it going !

Excellent Analysis but where there is a difference of Opinion ....... Orange Zone having Lenovo/Motorola.

Partners jump bandwagon on personal relations rather than a Solid Business paln of Due deligence about the Chinese counterpart.

Game changed as all OEM started to launch tjeir brands resulting is slow death of Indian brands.

Wow...

Great analysis with lots of insights to Indian mobile market. I am a privileged partner to be working with you since 2010 and for a micromax smartphone launch too; really happy that your experience is useful to so many of us and will definitely help in our decision making

Please continue your good work and guide us.

Thank you sir.

J. Madan

Jeevas Communications

Chennai

Excellent analysis along with ground reality figures Sir.It will help people and organisations to align their working with actual situation..

Well Said Sir ...there is more to come...Regards !!