Oppo India In The Soup?

- Ajay Sharma

- Nov 29, 2018

- 5 min read

Losses pile on. #OppoIndia’s MD Yi Wang quits.

Oppo launched its first phone in India in January 2014.

It was in February 2015, 1 year post its launch, I met one of their senior heads through a common friend at their then office on Sohna Road, Gurgaon. “Tony” was his name, if I remember it correctly. The discussions got around Oppo sales not growing to their expectations despite the investments.

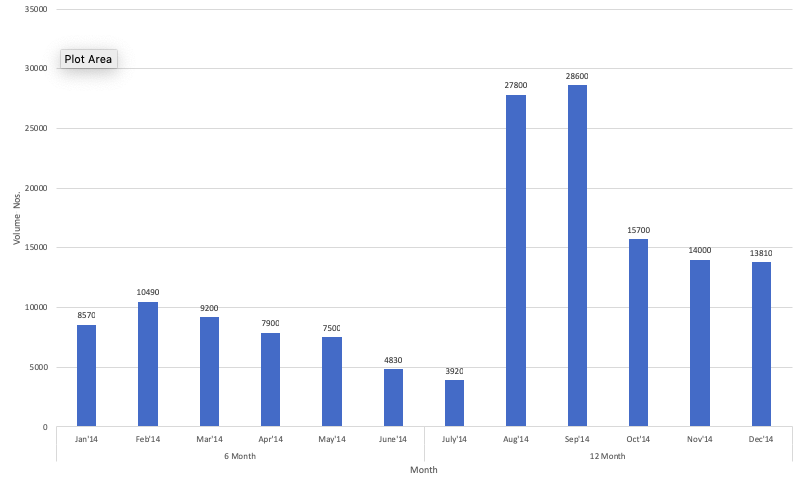

They had closed the calendar year 2014 with approx. 100k phones (as per my data taken from Zauba.com. See attachment 1), and wanted my inputs on next steps as the returns were not justifying the investments.

It was a short friendly meeting and the only message I conveyed to him was, take care of your first customer – the channel partners who are investing in your brand based on ROI. And the end consumer who’s buying your phone. Note: Customer is king! While I did praise their products, I also put forth the commitment they need to have towards keeping hygiene as key. The last and major point I highlighted to him was to give the confidence to the channel that the brand’s here to stay. Since Indians work a lot on trust levels, it’s of utmost importance to project an Indian face in front. All Korean and Taiwanese brands did have known Indian faces front ending their Indian business operations.

It is apparent that beyond my suggestions, they did their homework, designed a business strategy, executed it very diligently and came in the top 5 in the 1stquarter of 2017. The sudden growth was based on a business model of good quality innovative products with focussed feature highlights, attractive margins, way above normal supports to the channel. And all backed-up by huge marketing budgets. The Indian consumers got the bang for their buck by getting access to the latest technology (with Oppo’s robust R&D backend), and got it almost as the same time as the product release in China.

Oppo’s arsenal only got stronger, with the brand capitalising on the Indian consumers’ past experiences with Indian brands, with relation to product quality and after sales service, which was to date a displeasure. To add to this was the delayed launching of the latest technology products by the Indian brands and their wrong understanding of the market with respect to migration from 3G to 4G which left the Indian brands and their channel with loads of stocks which got cleared with loads of losses on either side. The Chinese were already prepared for this migration as China had started adopting 4G much earlier towards the end of 2013. It was a classic case of – “One brand’s gain was another brand’s loss.”

The market share and sales started growing with Oppo coming in the top 5, touching a double digit market share in Q1 of 2017. But then came the stage of the market share plateauing when the price and marketing supports (except for those committed for a long term) started getting slashed. This was essential to reduce the price gap with #Xiaomi – the challenger brand then – which was capturing a lot of eyeballs. The competition was offering the same specification product at a much lower price, and in order to sustain Oppo had to change the rules of the game. It was not possible for them to sell at the new adjusted price without cutting support expenses.

For share trends as per #Counterpoint, see attachment 2.

As it happens in most companies, rather than looking at how to grow sales, people first look at how to cut costs, and since margins and marketing were the biggest ones, these two took the maximum hit. The share started stagnating/declining. Of course, the losses widened owing to the price drop, the volumes stooped as well due to inability to acclimatize to the challenging market.

It was clear from day 1 that the expenses were disproportionate to sales, but the hope for higher market share/sales volumes to amortise the costs in the next 2-3 years, was immense.

Then the famous Hindi saying – “Vinashkale Vipreet Buddhi.”

Nothing against launch of Realme to take on Xiaomi, but then why say “#Realme from Oppo”. Or for that matter, bring Realme offline with a team with little or no experience in offline sales and understanding of the distribution channel.

And now the inevitable. Someone has to get crucified and the Oppo India MD is the one. (#BusinessStandard article. See attachment 3 )

So what went wrong?

They spent a lot of money, yes.

They reduced marketing expenses, alright.

But like my friend, Shubhodip Pal, Ex-CMO, #Micromax and #Samsung, who along with me was instrumental in taking on Samsung at one point, said to me just a couple of days back. “Did Oppo extract the full value out of the lessened spends, forget the initial spends with the kind of brand ambassadors and properties they have got? No! They could have done, and can still do a lot with what they are spending today – Especially when they have the biggest passion of India on their side – The Indian Cricket Team or the most wanted actress Deepika Padukone on their turf. What has the brand done with them till date? Or might I say “Ohno Oppo(turnity lost)!”

The newpaper article also talks about Oppo now borrowing money. A worrisome affair more after the launch of Realme which can cannibalise Oppo further, thereby further reducing their revenues – (Realme ASPs will be lower for similar specifications) and hence profits. Should we move Oppo from Green Zone to at least two levels below to Orange is the question now. Didn’t realise it will happen so fast. Though I did mention it in one of my earlier posts that Realme offline would affect Oppo.

While, yes, Xiaomi is selling same SKUs in both channels under the same brand name. One could question why should it therefore affect Oppo? Please do understand that Xiaomi’s approach has been very different. For starters, they created an unfulfilled demand for their product online through flash sales, making online as their A Game. The brand later sensed that their products were being sold offline as well with a slight premium, promising enough to officially launch the same in the offline trade too with a planned out timeline and defined share. They have played it smartly as of now. Whether they will be able to manage the same SKUs in both channels in the long term is a question. Let me assure you it will not be easy and Manu and team have to apply their minds day in and day out and execute the ideas that come out deftly to be able to not cannibalise their online or offline sales.

The newspaper article has the potential to create a lot of doubts in the minds of the channel on what lies ahead for Oppo. Well, they have to sit on the drawing board, and re-strategise on all fronts and reach out to the team and channel to give them the confidence that they may be down but definitely not out.

Growing from here will be a challenge with #Samsung on one side and the other top 4 brands like #Vivo, #Huawei which is struggling in offline but doing great online, #Motorola, #Transsion, moving in to fill in the gap. This might have a positive rub-off effect on a couple of Indian brands, not in terms of occupying the price slot lost by Oppo, but the faith and investments they’ll now see coming in, post a Chinese brand’s abrupt exit from India – #Comio – and now this. [Read my blog on Comio's exit from India here: https://bit.ly/2DUq0Z4]

Message to Vivo: The data does show that Vivo is also in losses but they are 1/3rd of Oppo and that there are no external borrowings being talked about. This is a positive sign. A slow and steady growth and not a decline is also a good sign. However, in this competitive industry one has to grow faster than the industry to be relevant. Online is therefore a necessity whether one likes it or not. How to play online without affecting offline will be key. Well a strategy around that is possible, only requires a careful study of the market.

With the emerging of oppo and vivo almost all industrial minds have question that is OPPO and VIVO making or losing money and I always asked this question with higher authorities of the industry and have doubt about survival of brand with this policy . Ultimately it happens and online player like amazon and flipkart are on the same way according to my small mind.

Truly a caution note to other brands. A very insightful article.

Sir rightly said, from last two quarters Oppo may lost Vision and Planning. That we feel in the market also. On other side Vivo always has one step ahead from Oppo in terms of Distribution, Operations, System Process and Timely New model launch...

Such a clear postmartem of oppo md exit.any step not taken in right direction will if not lead to debacle but atleast will give u swings on trajectory.nice information sir.

Rightly said Sir the marketing expenses and then launch of Realme powered by OPPO!!