India's Smartphone Market Enters Its Most Difficult Half: What H1 2026 Revealed and Why H2 Will Be Worse

- Ajay Sharma

- 9 minutes ago

- 8 min read

The headline number is not the story

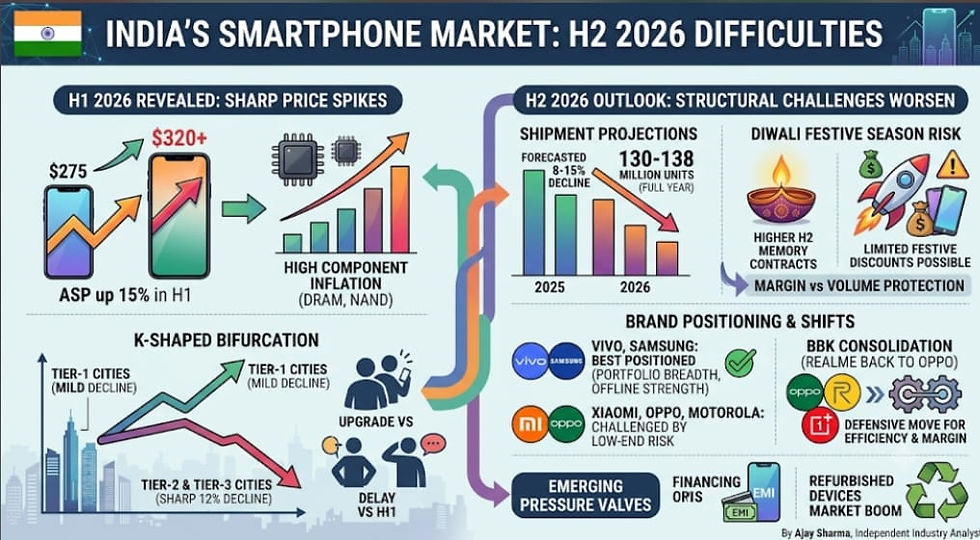

India's smartphone shipments are set to fall somewhere between 8 and 15 percent in 2026, depending on which agency you ask. Counterpoint Research pegs the decline at 10 percent year on year. IDC projects a steeper 12 to 15 percent fall to 130 to 132 million units, with average selling prices crossing $335 for the full year. CMR lands at the softer end, forecasting an 8 to 9 percent decline to 136 to 138 million units.

A 130-to-138-million-unit range is not analytical noise. It reflects real disagreement about how deep a supply-side shock cuts into a price-sensitive market, and how much of that shock consumers can absorb through financing rather than volume loss.

But the shipment number, whichever version you believe, is the trailing symptom. The actual story is what has been happening underneath it since January, and what the data suggests is coming in the back half of the year.

H1 2026: a market splitting along income lines

The first half of 2026 was defined by one number: smartphones became more than 20 percent more expensive year on year, driven almost entirely by DRAM and NAND cost inflation. Counterpoint's data shows average selling prices climbing from roughly $275 in H1 2025 to an estimated $320-plus in H1 2026, a 15 percent jump within a single half. That is an unusually sharp move for a market that has historically premiumized gradually, in single-digit annual increments.

The consumer response was not uniform, and that is the more interesting part. Tier-1 cities saw a comparatively mild 6 percent sales decline in the January to March quarter, cushioned by upgrade cycles and premium device purchases among consumers who either had the discretionary income to absorb higher prices or access to financing that made the increase invisible at the point of sale. Tier-2 and tier-3 cities were not so fortunate. Counterpoint points to a sharp 12 percent decline in these markets, roughly double the tier-1 rate, as price-sensitive buyers delayed upgrades, leaned harder on EMI and exchange offers, or simply stayed in the replacement cycle longer than planned.

This is the K-shaped bifurcation I have written about extensively, but H1 2026 gave it a sharper, more mechanical cause than usual. Omdia has quantified it precisely: the memory cost share within smartphone bill of materials nearly doubled in devices priced under $400 and rose by more than 100 percent in products above that threshold, comparing the first quarter of 2026 to the July-to-September 2025 window when component shortages first began biting.

That is the BOM cost asymmetry thesis in its clearest form yet. A flagship device absorbing a memory cost increase eats into an already generous margin. A sub-₹15,000 device absorbing the same dollar-value increase in memory costs often has its entire net margin erased. Brands serving that segment are left with two options, neither good: raise the retail price and lose volume, or quietly downgrade specifications, reverting to 4GB RAM configurations or slower storage types, and kill the very upgrade incentive that was driving replacement demand in the first place. Anecdotally, and consistent with what channel checks are showing, more brands are choosing the latter than they are admitting to publicly.

The H2 2026 precipice

If H1 was difficult, IDC is explicit that H2 will be harder. The forecast calls for second-half shipments falling to 68 to 70 million units, down from 82 million in H2 2025, a decline of more than 15 percent year on year. ASPs are expected to rise a further 20 to 25 percent in the same period. Stack that on top of an H1 that already saw a 20 percent-plus ASP increase, and India will likely close 2026 with average selling prices roughly 40 to 45 percent higher than they were entering 2025, on materially fewer units sold.

The reason H2 is structurally worse than merely a continuation of H1 comes down to contract timing. Brands typically lock in memory supply contracts months in advance. The favorable contracts that cushioned pricing through H1 were largely negotiated between November 2025 and the May-June 2026 window, before the full force of the DRAM and NAND spike hit spot pricing. Those contracts are now running out. Whatever brands negotiate for H2 delivery will reflect current, elevated spot prices, which means the price relief that partially protected H1 volumes disappears just as the market enters its highest-volume quarters.

This timing collision deserves more attention than it has received. India's festive season, spanning the Q3 and Q4 quarters around Dussehra and Diwali, typically accounts for 30 to 35 percent of the country's annual smartphone shipments. It is the period when brands traditionally compete hardest on discounting to capture volume. If festive-season inventory is being procured under freshly inflated H2 memory contracts, the arithmetic of a typical festive discount becomes difficult to sustain. India may be heading toward a genuinely unusual festive season: one where marquee launches carry list prices at or near their highest point of the year, rather than the customary discount cycle. Brands that have historically used the festive quarter to clear inventory and chase market share will instead be forced to choose between margin protection and volume protection.

Brand-by-brand: who is positioned to absorb this

CMR frames Vivo and Samsung as the best-positioned brands heading into this cycle, citing broad portfolios and strong mainline distribution as structural advantages. Xiaomi, Oppo, and Motorola are expected to perform relatively well by the same logic. This assessment is directionally sound, but it is worth stress-testing rather than accepting at face value.

Mainline distribution strength genuinely does buy resilience during a demand-side downturn, because offline channels retain relationship-driven, financing-assisted selling motions that are harder to replicate online. But offline depth does not automatically insulate a brand from a supply-side, BOM-driven shock. A brand's exposure to this cycle is really a function of where its volume concentration sits on the price curve, not how many stores it is present in.

A brand with a large share of its volume anchored in the sub-₹15,000 segment, which the data confirms is being hit hardest, carries real margin risk regardless of channel strength. Vivo and Samsung's relative advantage likely owes as much to their broader price-tier spread, with meaningful volume in mid and upper-mid segments that can absorb BOM inflation more comfortably, as it does to mainline presence per se.

The BBK consolidation: a defensive move read correctly

Set against this backdrop, the BBK Group's decision to fold Realme back into Oppo, alongside the convergence of ColorOS, OxygenOS, and Realme UI, reads less like routine portfolio tidying and more like a rational response to exactly the margin pressure this analysis describes. Running three separate operating system tracks and three semi-independent go-to-market organizations across Oppo, Realme, and OnePlus was always an expensive structure to maintain, one that made sense when component costs were stable and volume growth could fund the redundancy. In a BOM-inflation environment where every rupee of engineering and marketing overhead directly competes with margin preservation, that redundancy becomes a liability rather than a competitive asset.

Consolidating engineering resources, unifying software development, and rationalizing overlapping SKUs across what were effectively three volume-focused entry-to-mid brands is a direct efficiency response to a cost structure that no longer tolerates fragmentation. This is the BBK harvest thesis in practice: when the external environment stops rewarding multi-brand market coverage, the group behavior shifts toward consolidating share and defending margin rather than continuing to fund internal competition between its own labels.

The low-end inventory trap

There is a channel-level consequence to this cycle that shipment forecasts do not fully capture. The sub-₹15,000 segment is not simply experiencing softer demand; it is experiencing a deterioration in channel economics. Mainline retail in tier-2 and tier-3 India, general trade in particular, survives on rapid inventory turnover and thin per-unit margins. When brands raise entry-level price points or compress retailer commissions to protect their own margins against memory inflation, channel health absorbs the second-order impact.

If IDC's projected 15 percent-plus H2 shipment decline materializes, the more consequential downstream effect may be a wave of smaller multi-brand retail outlets scaling back inventory commitments or defaulting on credit lines extended by distributors, a channel-level stress that shipment data alone will not show until it shows up as store closures.

The 5G tax, now compounding

This shock has landed on top of an already-strained entry-level cost structure. For the past two years, the dominant industry narrative has been the push to bring 5G chipsets into the sub-₹12,000 segment, a transition that itself compressed margins because 5G modems and RF front ends carry an inherent cost premium over 4G equivalents. Layering 2026's memory price spike onto an entry-level BOM that was already absorbing a 5G tax has made the affordable 5G smartphone a genuinely endangered product category. Channel checks suggest brands are quietly reintroducing 4G SKUs at the lowest price tiers to preserve an affordable price anchor on shelves, a reversal of the technology curve that the industry spent two years pushing forward.

Financing has become the real product

As pricing pressure has intensified, EMI, exchange offers, and festive financing schemes have shifted from promotional tools to the primary mechanisms through which affordability is engineered for the Indian consumer. In practical terms, a meaningful share of India's smartphone market now behaves more like a consumer credit business than a hardware business. The brands most likely to defend volume through this cycle will not necessarily be the ones with the strongest camera systems or chipsets; they will be the ones with the deepest, most frictionless partnerships with NBFCs and captive financing platforms.

A brand that can structure a genuinely zero-down, 12/24/36 month scheme that converts a higher ASP into a digestible monthly instalment retains the tier-2 and tier-3 buyer. A brand that cannot do this loses that buyer to a competitor who can or loses them to the refurbished market entirely.

Refurbished devices as a pressure valve

This is where the refurbished and pre-owned smartphone segment becomes structurally relevant to this cycle rather than a peripheral side story. As new-device ASPs climb 40-plus percent in 2026 and entry-tier new devices either get more expensive or get quietly downgraded, a portion of price-sensitive demand that would previously have bought a new sub-₹10,000 device is being pushed toward the certified refurbished market instead.

Samsung's own move into organized refurbished retail is itself a tacit acknowledgment that the brand sees structural, not cyclical, demand for a lower-cost tier that its new-device pricing can no longer serve profitably.

The relationship runs in both directions. Rising new-device ASPs increase the pool of devices being traded in through exchange programs, which feeds refurbished inventory. At the same time, a growing organized refurbished channel gives brands a legitimate, margin-protected way to serve price-sensitive demand without discounting their new-device portfolio, which is precisely the kind of structural offload valve a market under sustained BOM pressure needs. Expect the refurbished segment's share of overall device transactions to expand faster in 2026 than in any prior year, not because used devices have become more desirable, but because new devices have become structurally less affordable at the exact income tier that previously anchored volume.

Online contribution under pressure

India's online smartphone channel grew on the back of aggressive platform-funded discounting, flash sales, and bank-partnership cashback offers, all of which depend on brands having enough margin headroom to fund promotional pricing. If H2 2026 genuinely becomes the discount-scarce festive season, this data suggests it could be, online's core value proposition to the price-sensitive buyer weakens precisely when it matters most.

Expect online's share of overall shipments to plateau or modestly contract in H2, with volume share shifting back toward mainline retail, where EMI-assisted, relationship-driven selling can still manufacture affordability even when list prices cannot move. This would be a meaningful, if likely temporary, reversal of a decade-long channel shift.

The nuanced read

The consensus reading of this cycle, that India's smartphone market is simply slowing down, is incomplete and somewhat misleading. Demand for connected devices in India remains structurally strong. What is happening instead is a forced re-sorting of the market by component economics rather than by consumer preference. A supply-side shock in memory pricing is acting as an involuntary filter, accelerating premiumization faster than India's middle-class income growth can organically support it, compressing the volume-anchor segment that has historically defined this market's scale, and rewarding balance-sheet depth over product differentiation.

The brands that emerge strongest in 2026 will not necessarily be the ones with the best specifications or the most aggressive marketing. They will be the ones with the financial capacity to treat this year as a deliberate market-share acquisition funded by short-term margin sacrifice, the operational discipline to consolidate cost structures the way BBK is doing with Oppo and Realme, and the channel sophistication to use financing and refurbished pathways as legitimate demand-preservation tools rather than treating them as afterthoughts. Everyone else will be managing decline rather than positioning for the recovery that follows it.

Comments