Market Share Lies, Policy Decides

- Ajay Sharma

- Feb 24

- 2 min read

Every agency report I’ve ever seen on the Indian smartphone industry starts the same way: a pile of numbers covering shipments’ data, market share, ASPs, channel splits, festive-season spikes, followed by a tidy conclusion that sounds smart for the future. That’s the problem.

Numbers are a rear-view mirror. They tell you what happened. They rarely tell you what will matter when the road bends. So in this PDF, I’ve intentionally stepped away from the usual “market share talks” and used the PESTEL framework to look at the industry the way it actually behaves in India: as a long-term contest of permission, trust, compliance, and leverage, and not just specs and pricing.

PESTEL is a simple idea: it’s the six invisible forces - Political, Economic, Social, Technological, Environmental, and Legal - that decide whether a brand gets to keep playing… even when it builds great products.

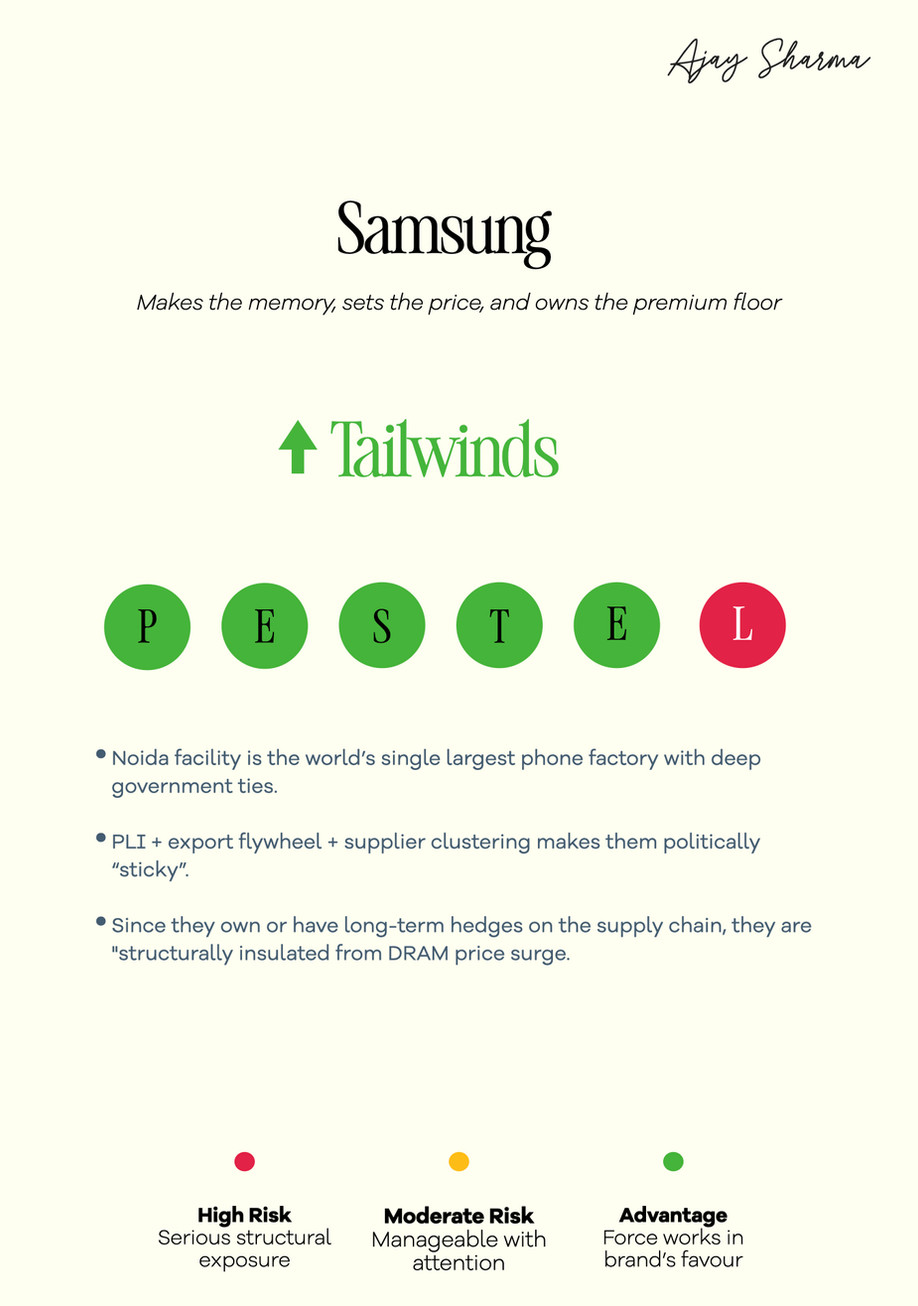

And while the deck covers brand-wise PESTEL, what jumps out is this: there are a few common forces that hit almost every player. For some as a headwind, some as a tailwind, depending on where they sit. Here are the big ones that repeat across the PDF, and also show-up clearly in the broader landscape:

Data privacy compliance is becoming non-negotiable. The DPDP Rules were notified in Nov 2025, with staggered enforcement that pushes the market toward major compliance readiness over the next ~18–24 months (often framed up to May 2027 for full readiness).

Component inflation is real and memory is the poster child: DRAM/NAND pricing has surged sharply, with research tracking ~80–90% jumps vs Q4 2025 in early 2026, and that pressure doesn’t hurt everyone equally; it squeezes the value end the hardest, forcing either thinner margins or visible spec cuts (storage tiers, camera stacks, display quality) to hold price points.

Competition scrutiny around exclusive launches and platform favoritism is a structural risk. The CCI spotlight on brands and e-commerce platforms isn’t just legal noise. It can rewrite go-to-market strategies, from launch exclusives and discounting to channel mix and partner terms.

E-waste + EPR compliance is no longer optional theatre. It’s cost, audit exposure, and operational discipline, especially painful for smaller brands that don’t have scale to amortize compliance.

India is premiumising, and that changes who wins. Social aspiration is pulling value share upward; brands with a credible premium story get pricing power and resilience, while “only sub-₹15k” brands feel every shock harder.

In India, policy leverage matters as much as the product. PLI alignment, local manufacturing footprint, and regulatory trust aren’t soft signals. They directly shape operational friction, time-to-market, and in some cases, a brand’s ability to stay in the game.

Tech maturity is now a baseline, not a differentiator. 5G is table stakes next layer. But, the real differentiator is who can fund it, ship it reliably, and support it without breaking trust.

That’s the thesis behind this work: Specs sell phones. But PESTEL decides who keeps selling them.

Comments